The Taiwanese Economy in August 2020

The COVID-19 did cause severe impacts on major economies, such

as the US and Europe. However, the second quarter of these advanced

economies were actually not as bad as they were projected earlier.

For example: The US Bureau of Economic Analysis adjusted its estimation

of second quarter GDP growth rate upward by 0.4 percentage points.

In addition, the Eurostat also upward revised its GDP growth predictions

for both the EU 27 and EA19 for the second quarter by 0.2 and 0.3

percentage points respectively. Despite of remaining uncertainties,

the domestic demands for the time being have obviously helped pick

up manufacturing as well as service composite indicators issued

by the Taiwan Institute of Economic Research (TIER) over again.

Taiwan's exports in August 2020 increased by 8.32% compared with

the same month of 2019 thanks to a strong market demand for ICT

parts and components. Regarding imports, Taiwan's imports in August

2020 increased by 23.9% compared with imports in August of 2019

due to the expansion of major semiconductor companies. On the cumulative

basis, Taiwan's exports and imports from January 1st till August

31st of 2020 actually grew by 1.54% and -0.12% compared with the

same period of previous year. The trade surplus during the period

stood at US$ 33.18 billion or increased by 11.89% on the year-on-year

basis.

Taiwan's consumer price index (CPI) decreased by 0.33% in August

2020 compared with the same month of previous year due to the still

decreasing global crude oil and commodity prices. The CPI has been

decreasing for 7 months in a row; however, the CBC trusts that there's

no deflation for now. The core inflation rate excluding prices of

the energy and food increased by 0.31% in August 2020. In addition,

the wholesale price index (WPI) decreased by 9.09% in August 2020

on the year-on-year basis due to the fact that commodity prices

dropped continuously. On the cumulative and year-on-year basis,

Taiwan's CPI and WPI from January 1st till August 31st of 2020 drop

by 0.27% and 8.43% respectively.

As for exchange rate, the NTD went somewhat weaker due to the relatively

stronger USD as well as flowing out capital. The NTD/USD stood at

29.53 in late August 2020 indicating a 0.08% depreciation. Regarding

the interest rate, it remained low and steady in August 2020 due

to the continued loose monetary operations by the CBC with respect

to the most recent CPI reading; the lowest and highest over-night

call rate in August 2020 stood at 0.079% and 0.088% respectively.

Business Outlook

The portion of manufacturing firms who perceived business were

better than expected in the target month was 35.3% or increased

by 6.0 percentage points compared with respondents who perceiving

better business in the previous month. The portion of those perceived

business were getting worse in the target month was 19.0% or decreased

by 1.5 percentage points than 20.5% perceiving worse business of

the previous month. The portion of manufacturing firms who perceived

business remained constant in the target month was 45.7% or decreased

by 4.5 percentage points compared with 50.2% perceiving constant

business in the previous month. Overall, manufacturing firms perceived

the business in the target month was somewhat more optimistic than

the previous month.

In addition, the portion of manufacturers who perceived business

would be better in the next six months was 27.7% in the target month

or increased by 7.6 percentage points than 20.1% feeling more optimistic

about the future in the previous month. The portion of firms who

perceived the economic outlook would be worsening was 23.8% or decreased

by 0.8 percentage points compared with 24.6% feeling rather pessimistic

about the future in the previous month. The portion of manufacturing

firms who perceived business remained constant in the next six months

stood at 48.5% or decreased by 6.8 percentage points compared with

55.3% feeling neutral about the business outlook one month earlier.

Overall, manufacturing firms perceived the business in the near

future was also more optimistic compared with the previous month.

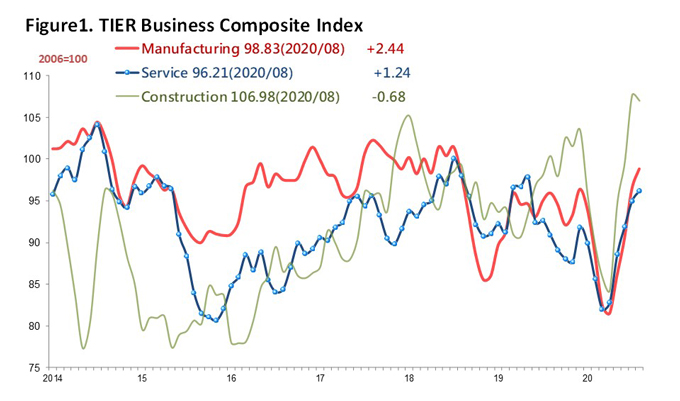

The manufacturing composite indicator for August 2020 adjusted for

seasonal factors on moving average, saw an upward correction, and

from a revision of as 96.39 points in July 2020 moved up to 98.83

points. Figure 1 shows an increase of 2.44 points, the fourth month

of consecutive increase.

The TIER service sector composite indicator for August 2020 adjusted

for seasonal factors on moving average also saw an upward correlation,

and from a revision of as 94.97 points in July 2020 moved up to

96.21 points. Figure 1 shows an increase of 1.24 points, the fifth

month of consecutive increase.

In addition, the TIER Construction Sector Composite Indicator for

August 2020 adjusted for the seasonal factors on moving average

saw a downward correlation, and from a revision of 107.66 points

in July 2020 went down to 106.98 points. Figure 1 shows a decrease

of 0.68 points, the first month drop after three months of consecutive

increase.

Forecast on Individual Industries

Following are manufacturers' sentiments that are industry-specific

in the monthly TIER surveys:

● Manufacturers' sentiments that have been in decline in the August

survey and are expected to deteriorate over the next six months

include:

Cutlery and Tools Manufacturing, Insurance.

● Manufacturers' sentiments that have been in decline in the August

survey, but are expected to improve over the next six months include:

Motor Vehicles Manufacturing, Real Estate Investment.

● Manufacturers' sentiments that have been in decline in the August

survey and are expected to remain sluggish over the next six months

include:

Leather, Fur and Allied Product Manufacturing, Chemical Products

Manufacturing, Machinery and Equipment Manufacturing and Repairing,

Electrical Appliances and Housewares Manufacturing, Bicycles Manufacturing,

Banks, Securities.

● Manufacturers surveyed who felt the August outlook was the same

as the previous month, but the outlook is expected to exacerbate

over the next six months include:

Petrochemicals Manufacturing, Petroleum and Coal Products Manufacturing,

Rubber Products Manufacturing, Screw, Nut Manufacturing, Electrical

Machinery, Supplies Manufacturing and Repairing.

● Manufacturers surveyed who felt the August outlook was the same

as the previous month, but the outlook is expected to improve over

the next six months include:

Frozen Food Manufacturing, Wood and Bamboo Products Manufacturing,

Plastics and Rubber Raw Materials, Cement and Cement Products Manufacturing,

Metal Structure and Architectural Components Manufacturing, Transport

Equipment Manufacturing and Repairing, Motor Parts Manufacturing,

Bicycles Parts Manufacturing, Education and Entertainment Articles

Manufacturing, Construction, Basic Civil Structure Construction.

● Manufacturers surveyed who felt the August outlook was the same

as the previous month and the trend is expected to continue for

the next six months include:

Manufacturing, Food, Slaughtering, Edible Oil Manufacturing, Flour

Milling and Grain Husking , Prepared Animal Feeds Manufacturing,

Yarn Spinning Mills, Fabric Mills , Paper Manufacturing, Industrial

Chemicals, Plastic Products Manufacturing, Non-metallic Mineral

Products Manufacturing, Porcelain and Ceramic Products Manufacturing,

Iron and Steel Basic Industries, Fabricated Metal Products Manufacturing,

Metal Dies, Industrial Machinery, Electrical Machinery, Electric

Wires and Cables Manufacturing, Electronic Machinery, Data Storage

Media Units Manufacturing and Reproducing, Wholesale, Telecommunication

Services, Transportation and Storage.

● Manufacturers' sentiments that have improved in the August survey

and is expected to deteriorate over the next six months include:

Glass and Glass Products Manufacturing, Restaurants and Hotels.

● Manufacturers' sentiments that have improved in the August survey

and is expected to remain upbeat over the next six months include:

Printing, Communications Equipment and Apparatus Manufacturing,

Motorcycles Manufacturing, Motorcycles Parts Manufacturing, Precision

Instruments Manufacturing.

● Manufacturers' sentiments that have improved in the August survey

and the trend is expected to continue for the next six months include:

Soft Drink Manufacturing , Textiles Mills, Apparel, Clothing Accessories

and Other Textile Product Manufacturing, Man-made Fibers Manufacturing,

Audio and Video Electronic Products Manufacturing, Electronic Parts

and Components Manufacturing, Retail Sales.

|